[Note: To view the entire chart, please click here. This article is an updated excerpt from a presentation Jay Friedman delivered at JCF’s CLE/CPE Seminar on June 6.]

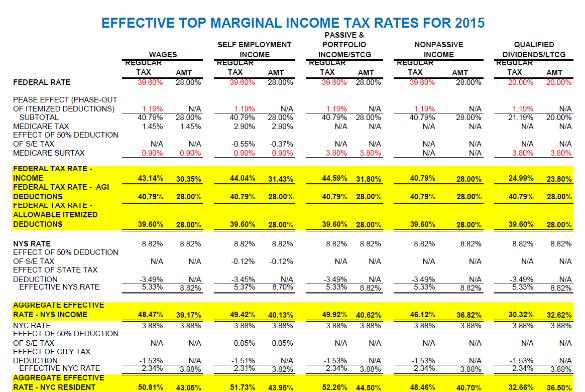

As a result of the enactment of the Medicare surtax, which is now applicable to both earned and investment income, effective individual income tax rates are now different for five types of income:

- Wages

- Self Employment Income

- Passive and Portfolio Investment Income (Including Net Short-Term Capital Gains)

- Nonpassive Income[1]

- Qualified Dividends and Net Long-Term Capital Gains

Depending on whether or not an individual is already subject to the alternative minimum tax (“AMT”), two varying effective marginal income tax rates may apply to each type of incremental income. Since an individual pays the greater of the regular and alternative minimum tax, the marginal rate for AMT purposes would apply until incremental ordinary income lifts an individual out of AMT; then the regular tax rate would apply to the remainder of such income.

Since there was virtually no change to AMT rates and substantial regular tax rate increases, many taxpayers who have regularly been subject to AMT will no longer be subject to it. Those who still are can be lifted out of it much more quickly than before as a result of incremental ordinary income. Since regular and AMT rates for qualified dividends and long-term capital gains are still identical, high income taxpayers whose income is largely comprised of this type of income may remain subject to AMT, especially if they reside in states with a significant income tax or have significant real estate taxes, investment management fees and/or other AMT preferences and adjustments.

While much has been published about the change in federal tax rates, there has been little focus in the media about aggregate marginal tax rates that are inclusive of state and local taxes and the more extreme disparity that now exists between regular and AMT rates. With careful planning, substantial savings can be realized by planning for the timing and amount of the various types of income to achieve lower tax rates.

The accompanying chart reflects both the current top regular and AMT aggregate effective marginal rates that are applicable to all five types of income for residents of states without an income tax such as Florida, and for residents of New York State, New York City, New Jersey, Connecticut and California.

Passive and investment income is taxed at the highest rates for federal income tax purposes, with New York City and California residents having combined tax rates as high as 52% or more on incremental income. The aggregate effective marginal rate on virtually all other ordinary income is roughly 45% to 50% for all other states listed. Aggregate effective marginal capital gain rates can range from around 30% to 37% for AMT taxpayers, depending on the state or city of residence.

Due to the Medicare surcharge and return of the “Pease limitation” that phases-out itemized deductions, effective marginal rates applicable to most types of income are now higher than rates applicable to deductions from gross income. This differential is even more substantial for residents of high tax states that do not allow itemized deductions, and states like New York, which disallows all itemized deductions other than 50% or 25% of charitable donations for taxpayers with incomes over certain thresholds. Accordingly, careful planning with regard to charitable and other deductions is also more important than ever before. The disparity in rates between investment or passive income and itemized deductions is close to 10% for most of the states reflected in the chart, and even slightly more than 10% for residents of New Jersey. It is close to 11% for residents of New York City with New York adjusted gross income in excess of $10,000,000.

The footnotes at the bottom of the chart indicate that rates are based on an assumption that, prior to the effect of any incremental income or deductions, an individual already has enough ordinary income to cause the highest federal, state and local marginal income tax rates to apply in each jurisdiction. It should be noted, however, that for New York State, the top rate of 8.82% first becomes effective at $2,000,000 of New York taxable income. New York’s rate applicable to income below that level is not more than 6.85%.

[1] Nonpassive income not subject to the Medicare surtax includes, but is not limited to pension, annuity and IRA income, rental income of a real estate tax professional, and ordinary income of an active S corporation shareholder.